Fintech and Climate Resilience in Banking: Navigating Risk and Opportunity

DOI:

https://doi.org/10.35945/gb.2026.21.002Keywords:

Bank risk management, fintech, climate-related financial risk, blockchain, green financeAbstract

Climate-related financial risks, encompassing both physical and transition dimensions, present an escalating threat to global financial stability, necessitating sophisticated risk management responses from the banking sector. This literature review synthesizes existing academic and industry research on the intersection of financial technology (Fintech) and bank climate risk management. The review establishes Fintech’s critical role in enhancing banks’ capacity to assess, monitor, and mitigate these complex risks through solutions such as Artificial Intelligence (AI), Machine Learning (ML), blockchain, big data analytics, and digital platforms for green finance. It examines methodologies, identifies key trends, and analyzes evolving perspectives from academic scholarship and industry practice on integrating climate risk into operational and strategic frameworks. Furthermore, this work investigates the challenges and limitations confronting fintech adoption, including data scarcity, regulatory hurdles, technological integration barriers, and ethical considerations such as algorithmic bias and the threat of “greenwashing”. The review concludes by highlighting emerging best practices and innovative approaches, synthesizing gaps in the existing literature, and proposing a research agenda designed to inform researchers, policymakers, and financial institutions. This foundation enables these stakeholders to navigate this dynamic landscape, contributing to a more resilient and sustainable financial system.

Keywords: Bank risk management, fintech, climate-related financial risk, blockchain, green finance.

JEL Classification: G32, G20, Q54, O31, Q56.

Introduction

Global economic losses from climate-related disasters have surged to over $200 billion annually in recent years, with projections indicating a potential 10% reduction in global GDP by 2050 under severe climate scenarios.[1] This reality establishes a critical imperative for the banking sector: climate risk management is a central pillar of financial stability. In this perspective, climate-related risks must be understood not only as environmental concerns, but also as direct threats to banking resilience and financial stability[2]. The financial system is exposed to climate-related risks through its lending, investment, and insurance activities.[3] Addressing these challenges requires enhanced data and analytical capabilities, robust supervisory frameworks, and international cooperation.[4] Climate-related risks manifest in distinct, interconnected typologies:

Physical Risks: These stem from the direct impacts of climate change, such as extreme weather events, rising sea levels, and chronic shifts in temperature and precipitation patterns.[5] For banks, physical risks threaten collateral values, increase loan defaults, and disrupt operational continuity. Examples include real estate portfolios exposed to recurrent flooding or agricultural loans vulnerable to prolonged droughts.[6]

Transition Risks: These arise from the transition to a low-carbon economy, including policy changes (e.g., carbon pricing), technological innovation, and shifts in market sentiment and consumer preferences.[7] Such risks can lead to stranded assets, reduced profitability for carbon-intensive sectors, and increased credit and market risks for banks with exposure to these industries.

Liability Risks: These stem from legal claims against entities for climate-related damages or insufficient climate action. Banks face indirect liability through their financing activities for companies exposed to such litigation.

These risks are not externalized costs; they are internalized as direct financial exposures, altering asset valuations and balance sheet stability. The “tragedy of the horizon”,[8] where long-term climate impacts conflict with short-term financial planning, creates a key tension requiring immediate attention.

Fintech, encompassing Artificial Intelligence (AI), Machine Learning (ML), blockchain, big data analytics, and digital platforms, emerges as a transformative force in navigating these complex financial risks. More broadly, this role reflects the wider transformation of financial services through fintech-driven innovation ,disruption, and digital reconfiguration[9]. Technological innovation, including big data analytics and AI, plays a significant role in improving climate-related risk assessment, though these tools are still nascent in this application area.[10] Fintech enhances data collection, processing, and risk modeling, improving financial institutions’ ability to monitor and mitigate climate-related financial risks.[11] This connection between the urgency of climate risk and the necessity of technological innovation forms the foundational premise of this literature review. While Fintech offers capabilities for strengthening climate risk management, its full potential can only be realized by systematically addressing data fragmentation, regulatory incoherence, and the complexities of technological integration, necessitating a concerted global effort. This literature review therefore aims to examine how fintech tools can strengthen bank’s capacity to identify ,assess, and mitigate climate-related financial risks, while also highlighting the regulatory, operational, and ethical challenges associated with their adoption.

1. Literature Review and Theoretical Framework

1.1. Foundational Frameworks for Climate Risk in Banking and Finance (2018-2021)

Early scholarship between 2018 and 2021 established the conceptual groundwork for understanding climate-related financial risks in banking, predating the widespread discussion of fintech solutions. This period was characterized by a push to integrate climate considerations into financial stability mandates, with researchers identifying climate change as a systemic risk requiring new regulatory paradigms.[12] An initial focus was on developing macroprudential policies to manage these novel risks and steer investments toward a low-carbon economy. Concurrently, scholars began dissecting the specific transmission channels through which climate change affects financial stability, such as the risks posed by declining “sunset” industries heavily reliant on fossil fuels. These studies argued that the transition to a low-carbon economy could trigger abrupt asset revaluations and defaults, threatening the entire financial system. Methodologically, this era saw proposals for climate stress tests to gauge institutional resilience and the advocacy for a ‘precautionary approach’ to policymaking, which argues that the radical uncertainty of climate impacts necessitates proactive regulatory action even without complete scientific certainty. Collectively, these works framed climate change not merely as an environmental issue but as a core threat to financial stability, creating the intellectual and regulatory justification for the technological interventions that would follow.[13]

1.2. The Dual Role of Fintech in Climate Risk and Resilience (2022-2025)

Building on the foundational risk frameworks, the literature from 2022 to 2025 shifts to the practical, yet complex, role of fintech in addressing climate challenges. This contemporary body of work highlights a significant tension: while fintech is often lauded for its potential to enhance climate resilience, recent empirical work also suggests it can significantly amplify climate risk in financial markets. Some studies illustrate how fintech can cushion firms from the adverse impacts of climate risk and improve resilience against climate shocks for both households and companies. More specifically, green fintech solutions are seen as critical for improving sustainability, mitigating risks, and achieving financial stability. These technologies are positioned as key enablers of sustainable finance, capable of accelerating the shift to a carbon-neutral economy. This broader interpretation is consistent with recent scholarship that situates fintech within a wider nexus linking climate challenges , green finance , digitalization ,and environmental quality[14]. For instance, AI and blockchain are identified as tools that can improve the efficiency of green financing, enhance risk management related to ESG events, and increase the transparency of sustainable transactions. However, research also cautions that integrating fintech for sustainability is not straightforward, with one study on the Indonesian banking sector finding that fintech adaptation had a limited direct impact on sustainability performance, pointing to the need for better regulatory frameworks and strategic implementation. This duality underscores that while fintech offers powerful instruments for building a climate-resilient banking system,[15] its deployment requires careful management to avoid exacerbating the high risks it aims to mitigate.

2. Fintech Solutions: Advanced Analytics, Transparency, and Green Finance

2.1. Advanced Analytics, Transparency, and Green Finance Facilitation

Fintech solutions offer transformative capabilities for enhancing climate risk management in banking, moving beyond static risk assessment to dynamic, data-driven approaches. These tools address the “Climate Risk Imperative” by providing granular insights and fostering greater transparency in green finance.[16]

Artificial Intelligence and Machine Learning: Advanced Data Analytics and Modeling

Artificial Intelligence (AI) and Machine Learning (ML) are fundamental to significant advancements in climate risk assessment. These technologies process vast, disparate datasets, enabling predictive modeling of physical risks and granular analyses for transition risk scenarios.

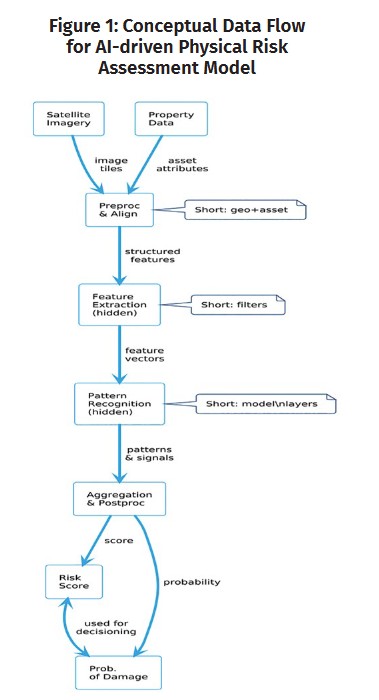

Physical Risk Modeling. AI/ML models downscale global climate projections, such as CMIP6, to regional and asset-level resolutions, sometimes as fine as 90 meters.[17] These models integrate historical climatic data with specific asset characteristics, like property elevation or construction materials, to project future physical damages from hazards such as floods or wildfires. Satellite imagery and geospatial data serve as critical inputs, facilitating near-real-time monitoring and dynamic risk adjustments.[18] For instance, SatSure’s “SatSure Sage” platform and CropIn’s “SmartRisk” platform employ ML with satellite and weather data to assess agroclimatic risk for Indian banks, correlating crop performance with historical risks to inform loan underwriting and portfolio monitoring.[19] The conceptual data flow for AI-driven physical risk assessment transforms raw environmental and asset data into actionable risk scores, as illustrated in the following diagram.

Transition Risk Scenario Analysis. AI-driven sentiment analysis, particularly through Natural Language Processing (NLP) models, parses unstructured data from regulatory texts, corporate climate disclosures (e.g., TCFD reports), and news articles. U-Reg’s NLP-based algorithms, for instance, process vast quantities of ESG disclosure data to identify inconsistencies and extract insights on policy foresight, litigation risk indicators, and market sentiment shifts.[20] These models enable banks to anticipate the financial impact of decarbonization policies and market shifts.

Blockchain and Distributed Ledger Technology: Transparency and Verifiability

Blockchain and Distributed Ledger Technology (DLT) enhance transparency and verifiability in sustainable finance, addressing concerns such as greenwashing and data integrity.[21]In this regard,the literature on greenwashing provides an important framework for understanding how misleading environmental claims can weaken the credibility of sustainable financial innovation[22].

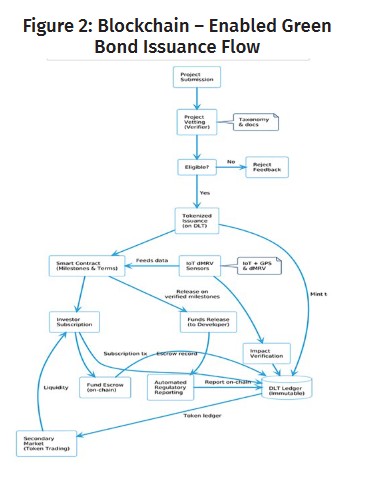

Green Bonds and Impact Verification. Blockchain creates immutable records of green bond issuance, ensuring funds are allocated to stated environmental projects. Fever Tokens, for example, proposes an open-source solution for on-chain monitoring throughout the life cycle of tokenized green bonds, adhering to ICMA’s Green Bond Principles and the EU’s Green Bond Standard.[23] This significantly boosts transparency and investor trust by providing verifiable impact metrics recorded on a distributed ledger.

Carbon Credit Markets. Blockchain technology improves the tracking of carbon credits, providing an auditable history for each credit’s origin and transaction[24], and offers a blockchain-driven platform for trading, clearing, and settlement of carbon credits and ESG assets, eliminating greenwashing and double-counting through robust data verification and traceability.[25] Triangle’s Asset OS platform links asset data with verifiable information using blockchain, facilitating TCFD reporting compliance and enabling the minting of fungible carbon credits.[26]

This diagram illustrates satellite imagery and property data as inputs, hidden layers for feature extraction and pattern recognition, and outputs as a risk score or probability of damage.

Digital Platforms and RegTech: Green Finance Facilitation and Compliance

Digital platforms and RegTech solutions facilitate green finance flows and automate climate-related disclosures.

Green Finance Platforms. These platforms direct capital toward climate-aligned initiatives. Examples include crowdfunding platforms like Abundance Investment for renewable energy projects, and investment marketplaces such as STACS’ ESGpedia. ESGpedia aggregates and harmonizes sustainability data, creating standardized ESG company profiles mapped to financial sector regulatory formats.[27] This enhances market efficiency and transparency in sustainable investment.

RegTech for Climate Reporting. RegTech solutions automate climate-related disclosures and ensure compliance with evolving regulatory mandates. U-Reg’s U-Green module leverages AI and RegTech to address fragmentation and standardization challenges in ESG reporting, processing unstructured data at scale through NLP-based algorithms.[28] These tools streamline the complex process of reporting climate-related financial exposures, reducing administrative burdens on banks.

Gaps in Literature. Despite these advancements, significant gaps persist in the literature. Comprehensive research on the long-term efficacy and robustness of AI/ML models under deep uncertainty remains limited. Interoperability standards for diverse Fintech solutions and climate data platforms require further development. Scalability challenges for blockchain applications in large-scale financial markets, particularly for tokenized assets, are not fully resolved. The “Crisis of Actionable Data”, characterized by pervasive deficiencies in granularity, standardization, and verifiability, implicitly constrains the full potential of these advanced tools, leading to an “Algorithmic Greenwashing” paradox if transparency is not rigorously enforced.[29] These identified gaps directly inform the subsequent discussion of implementation challenges.

- Integrating Fintech and Confronting Limitations

3.1. Integration Dynamics and Foundational Impediments

The integration of Fintech solutions into banking operations for climate risk management reveals a “translation gap” between academic ideals and industry pragmatism. Academic research often prioritizes theoretical completeness, aiming for universal models and long-term systemic impact. Industry, by contrast, operates under immediate pressures of shareholder value, operational efficiency, and the constraints of legacy systems. This divergence means that while academia may critique inherent simplifications in industry climate models, industry prioritizes solutions readily integrated into existing risk frameworks with minimal disruption and cost. This gap impedes Fintech’s transformative potential.

This flowchart illustrates the stages from project vetting and tokenized green bond issuance on a DLT to fund allocation based on smart contracts, impact verification via IoT sensors, and automated regulatory reporting.

The journey towards climate resilience through Fintech is fraught with significant challenges, stemming from pervasive data scarcity, regulatory hurdles, technological integration barriers, and multifaceted ethical considerations. These challenges constrain Fintech capabilities and demand a utility-driven research agenda.

Data Scarcity, Quality, and Standardization. The most fundamental impediment is not merely a lack of data, but a “Crisis of Actionable Data” characterized by deficiencies in granularity, standardization, and verifiability. The Network for Greening the Financial System (NGFS) found that 514 out of 1,262 raw data items lacked a linked source, with the largest gaps in biophysical impact, emissions, and geospatial data types.[30] This directly limits the usability of metrics for physical vulnerability and transition sensitivity.

Methodological inconsistencies further compound this problem. Estimating Scope 3 emissions, for example, is hindered by varying boundary definitions, reliance on different emission factor databases, and diverse allocation methods across complex supply chains. This results in incomparable and often unreliable data for financial institutions.[31] Approximately 39% of all climate-related data items are based on estimations, with less than a quarter being official statistics or verified.[32] This reliance on unverified or estimated data undermines the accuracy of Fintech-driven risk assessments, creating an “illusion of precision” that can lead to mispriced assets.

Regulatory Hurdles and Policy Lag. The fragmented and evolving nature of global climate finance regulation creates significant uncertainty, hindering Fintech innovation and adoption. Jurisdictions exhibit varying approaches; the EU’s fragmented data sharing standards under GDPR, for instance, complicate cross-border climate data aggregation.[33] Central banks also issue varying levels of prescriptive technological guidelines, from the Bank of England’s detailed expectations to the OCC’s higher-level principles.[34] This “regulatory lag” means frameworks struggle to keep pace with rapid technological evolution.

Model validation for AI/ML solutions presents further complexities. Demonstrating model explainability (XAI) and robustness under diverse climate scenarios becomes a formidable task given the “black-box” nature of some advanced algorithms. Data residency requirements for global financial operations mandate that climate data remains within specific national borders, complicating the deployment of cloud-based Fintech solutions.

Technological Integration Barriers. Banks face significant challenges in integrating cutting-edge Fintech with entrenched legacy IT systems. The inertia of monolithic core banking platforms resists seamless API integration, creating data silos and inefficient workflows. Harmonizing disparate data formats from various Fintech providers adds another layer of complexity. Pervasive talent gaps also exist, with a scarcity of data scientists possessing both financial and climate expertise, and risk managers capable of interpreting complex AI-driven climate analytics.

Ethical and Reputational Considerations. Ethical dimensions, while not directly financial, generate material financial risks for banks. “Climate washing”, where overstated climate credentials inflate valuations, exposes banks to sudden devaluations, regulatory penalties, and reputational damage. Data biases in AI/ML models, if trained on historical data from predominantly developed economies, could misallocate capital by underestimating physical risks in emerging markets or overestimating transition risks for specific sectors, exacerbating existing inequalities. Data privacy breaches of climate-related information expose banks to legal and reputational risks. Algorithmically unfair risk assessments can lead to legal challenges and regulatory penalties for discriminatory practices. This “Algorithmic Greenwashing” paradox highlights how tools designed for transparency can inadvertently facilitate deception.

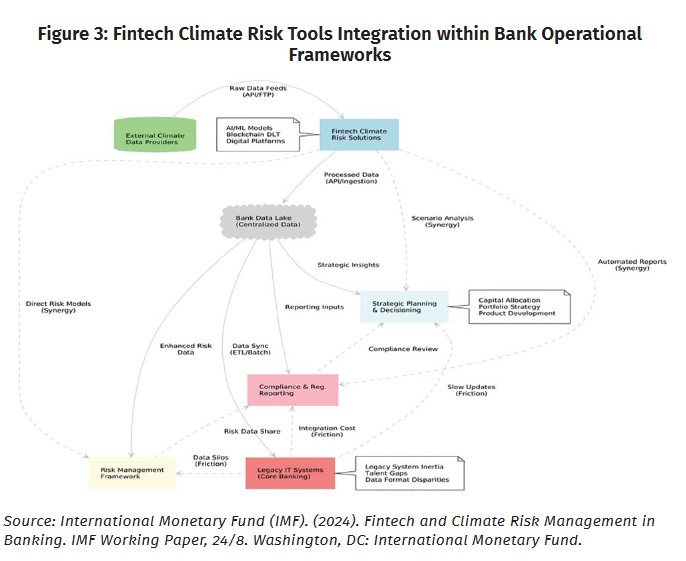

This flowchart details the integration points of Fintech solutions (e.g., API integration, data lake ingestion) within a bank’s existing risk management, compliance, and strategic planning processes, highlighting potential points of friction and synergy. It clarifies operational complexities.

The challenges outlined above necessitate a structured approach to addressing data quality and consistency.

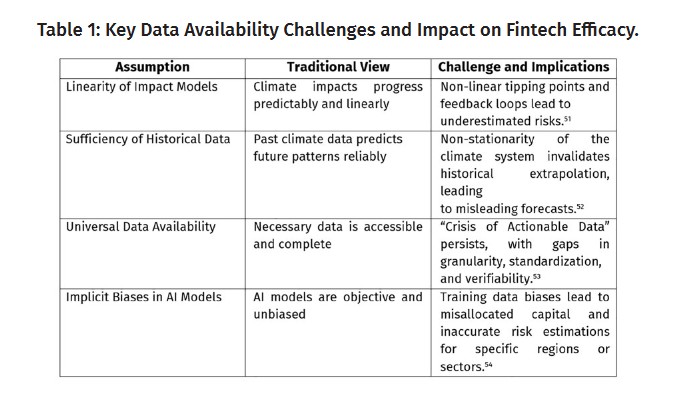

This table summarizes the core data availability challenges confronting Fintech solutions in climate risk management and their direct impact on the efficacy of these technologies.

Gaps in the literature related to integration costs, the effectiveness of various regulatory sandboxes, and the full scope of systemic risks arising from Fintech dependencies demand further investigation. These impediments, from data fragmentation to regulatory incoherence, underscore the imperative for a coordinated, multi-stakeholder effort to bridge the chasm between technological potential and practical implementation.

4. Emerging Practices and Future Trajectories

Innovative Approaches and Best Practices

The banking sector’s pursuit of climate resilience, despite formidable impediments, drives the emergence of innovative Fintech approaches and best practices. These solutions enhance capabilities and directly address many of the implementation challenges previously discussed, offering pathways to optimize climate risk management.

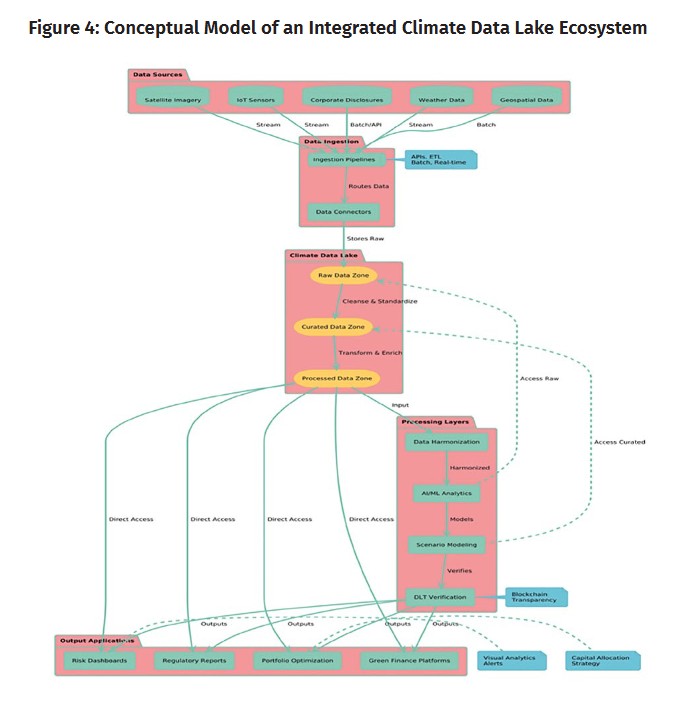

Integrated Climate Data Lakes. Data fragmentation, a pervasive challenge, finds mitigation in the development of integrated climate data lakes. These initiatives involve consortia and collaborative efforts where multiple banks and climate science communities pool anonymized climate-related data. Platforms like Dataland, a neutral, open-source data platform, exemplify this approach, focusing on company-specific raw data aligned with regulatory disclosure standards.[35] Dataland operates on principles of integrity, disclosure, transparency, accountability, neutrality, and collaboration, overcoming data availability gaps, reliability issues, and high acquisition costs.[36] This collaborative infrastructure acts as a public good, reducing the prohibitive costs of data acquisition and integration for individual banks and fostering collective intelligence.

This diagram illustrates the various data sources (e.g., satellite, IoT, corporate disclosures), data ingestion points, processing layers (e.g., AI/ML analytics), and output applications (e.g., risk dashboards, regulatory reports) within an integrated climate data lake, clarifying the flow and aggregation of information.

Open-Source Climate Risk Modeling Platforms. To counter the “black-box” nature of proprietary models and mitigate “Algorithmic Greenwashing”, open-source climate risk modeling platforms emerge from academic institutions and non-profits. Initiatives such as OS-Climate provide transparent and auditable tools for risk assessment, fostering trust and enabling collaborative development of methodologies.[37] These platforms enhance model explainability and allow for independent validation, addressing concerns about algorithmic bias and the robustness of climate projections.

Digital Twins of Physical Assets. Innovative approaches extend to the creation of digital twins of physical assets. Pilot studies demonstrate how virtual replicas of buildings or infrastructure integrate climate models to simulate future flood, heatwave, or other climate impacts.[38] This allows banks to assess collateral resilience dynamically, providing granular, forward-looking insights into asset vulnerability. For example, Triangle creates blockchain-based digital twins of real-world assets linked to climate data, facilitating the reporting of financed emissions.[39]

Blockchain-Enabled Platforms for Green Energy. Blockchain technology facilitates “Green Finance” through platforms enabling fractional ownership in green energy projects and enhancing the transparency of green financial instruments. Powerledger, for instance, utilizes blockchain for peer-to-peer renewable energy trading, democratizing access to green energy markets. FeverTokens proposes on-chain monitoring for tokenized green bonds, adhering to established principles like ICMA’s Green Bond Principles and the EU’s Green Bond Standard.[40] This boosts transparency and trust in green investments, directly combating greenwashing by providing verifiable impact metrics, and offers a blockchain-driven platform for carbon credit trading, ensuring traceability and preventing double-counting.[41]

These emerging practices demonstrate Fintech capabilities actively optimizing climate resilience. They provide concrete examples of progress, directly addressing the “Crisis of Actionable Data” through integrated data initiatives and mitigating the potential for “Algorithmic Greenwashing” through transparent, open-source models. The continued development and adoption of these innovative approaches are crucial in building a more robust and sustainable financial future.

4.2. Uncharted Territories and Systemic Re-evaluations

The landscape of Fintech and climate risk management reveals unexplored interconnections and necessitates a critical re-evaluation of underlying assumptions. Existing literature’s “white spaces” highlight nascent research areas and systemic vulnerabilities unaddressed by current approaches.

4.3. Unexplored Interconnections and Nascent Research Areas

Novel conceptual links include direct feedback loops between climate-induced physical risks and automated portfolio adjustments. AI’s real-time geospatial data processing could trigger immediate re-evaluations of mortgage-backed securities as flood risks intensify.[42] This extends financial engineering principles to novel climate data streams, offering dynamic risk management beyond traditional, lagging indicators.

Nascent research areas include the systemic risks arising from the interconnectedness of climate-aware Fintech solutions. A single climate data provider’s AI model failure could precipitate cascading failures across multiple financial institutions, leading to widespread mispricing of climate risk. The concentration of climate data provision within a few specialized Fintech firms creates a “barbell” risk structure, where failure in one provider could have systemic implications; this is a concern echoed by the Bank for International Settlements (BIS) regarding critical infrastructure.[43]

Quantum computing’s potential to accelerate complex climate scenario modeling draws from theoretical computer science papers outlining its capability for exponential speedup in optimization problems.[44] Bio-mimicry principles for resilient investment strategies, supported by ecological economics literature, suggest novel financial products and portfolio constructions emulating nature’s adaptive capacities.[45]

4.4. Re-evaluating Underlying Assumptions and Systemic Implications

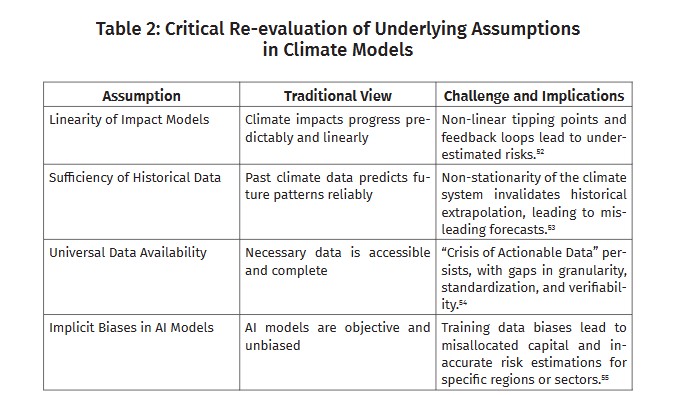

A critical re-evaluation of underlying assumptions in climate models is necessary. The “assumption of linear climate impact models” is challenged by research highlighting non-linear tipping points and feedback loops within the climate system.[46] These non-linear dynamics render linear projections inadequate. The “sufficiency of historical data” for predicting future climate risks is challenged by palaeoclimate studies and extreme event attribution science, which demonstrate unprecedented climate shifts.[47]

Implicit biases in model training data, particularly when AI models are trained on incomplete or geographically skewed climate data, can misrepresent risks for underrepresented regions. This leads to mispriced assets and potential financial instability.[48] The “assumption of universal data availability” is challenged by the NGFS report, which quantifies significant data gaps, identifying 514 out of 1,262 raw data items as unlinked to a source.[49]

The systemic implications of Fintech adoption include a significant shift in the competitive landscape. The BIS notes a potential “barbell” market structure, where large, technologically advanced players dominate climate risk analytics, potentially marginalizing smaller banks that lack the necessary investment capacity.[50] This concentration could create new systemic vulnerabilities should these dominant providers experience disruptions, thereby impacting regulatory oversight. A critical re-evaluation of underlying assumptions in climate models is summarized in the table below. This table summarizes the essential re-evaluation of underlying assumptions in climate models, contrasting traditional views with challenges and implications for financial risk assessment.

These “Gaps in Literature” and “Unexplored Interconnections” necessitate future research, justifying a “Utility-Driven Research Agenda”. Current understanding and technological application remain insufficient for navigating the complex future of climate resilience in banking.

The financial sector’s pursuit of climate resilience, while relying heavily on Fintech innovation, navigates a landscape marked by significant data gaps, fragmented regulatory environments, and the inherent inertia of legacy systems. While Fintech solutions offer granular risk assessment and enhanced transparency in green finance, their widespread adoption encounters fundamental limitations.[55] This necessitates a radical rethinking of data governance, cross-border supervisory cooperation, and a re-evaluation of the implicit assumptions guiding current climate models. The optimal future state involves a symbiotic ecosystem where financial institutions, Fintech innovators, and regulators collaboratively establish standardized, interoperable, and ethically sound frameworks, moving beyond isolated solutions to build a robust and anticipatory climate-resilient financial architecture.

Conclusion

The escalating threat of climate-related financial risks has emerged as a pivotal concern for global financial stability. This literature review has synthesized a comprehensive body of research concerning the intersection of financial technology (Fintech) and climate risk management within the banking sector. The findings underscore the critical role that Fintech can play in enhancing the banking industry’s capacity to assess, monitor, and mitigate the multifaceted risks posed by climate change. Through the deployment of advanced technologies such as Artificial Intelligence (AI), Machine Learning (ML), blockchain, big data analytics, and digital platforms for green finance, banks can navigate the complexities of climate risk more effectively.

Fintech’s integration into climate risk management represents a transformative shift in how banks can operate in an increasingly volatile environment. The literature indicates that AI and ML can significantly improve risk assessment processes by enabling more accurate modeling of climate-related financial risks. These technologies facilitate the analysis of vast datasets, allowing banks to identify patterns and predict potential impacts of climate change on their portfolios. Furthermore, big data analytics can enhance monitoring capabilities, providing real-time insights into environmental changes and their potential financial implications.

Blockchain technology also offers promising solutions for transparency and traceability in green finance initiatives. By creating immutable records of transactions, blockchain can help mitigate concerns related to greenwashing—the practice of presenting an organization as more environmentally friendly than it truly is. This transparency is essential for building trust among stakeholders and ensuring that investments genuinely contribute to sustainability goals.

Despite the promising potential of fintech in addressing climate-related financial risks, several challenges and limitations persist. One of the most significant barriers is data scarcity. The availability of high-quality, granular data on climate impacts remains limited, particularly in developing regions. This scarcity complicates risk assessment and modeling efforts, hindering banks’ ability to make informed decisions.

Regulatory hurdles also pose a considerable challenge to fintech adoption in climate risk management. The rapidly evolving regulatory landscape surrounding climate-related disclosures and sustainability reporting can create uncertainty for financial institutions. Banks must navigate these complexities while ensuring compliance, which can be resource-intensive and may stifle innovation.

Technological integration barriers further complicate the adoption of fintech solutions. Many banks operate on legacy systems that may not be compatible with new technologies. This mismatch can hinder the seamless implementation of advanced analytics and AI, limiting the potential benefits that these technologies can offer.

Ethical considerations, particularly concerning algorithmic bias and the risk of greenwashing, must also be addressed. The deployment of AI and ML in climate risk management necessitates a careful examination of the underlying algorithms to ensure they do not inadvertently perpetuate biases or misrepresent environmental impacts. As banks increasingly rely on these technologies, establishing robust ethical guidelines and accountability mechanisms will be essential to maintain credibility and public trust.

Considering these challenges, the literature review has illuminated several emerging best practices and innovative approaches that can guide banks in their climate risk management efforts. Collaboration between financial institutions, technology providers, and regulatory bodies is paramount. By fostering partnerships, stakeholders can share expertise, resources, and data, ultimately enhancing the efficacy of fintech solutions in addressing climate risks.

Furthermore, the establishment of industry standards for climate risk assessment and reporting can facilitate greater consistency and comparability across financial institutions. Such standards would not only aid banks in aligning their practices with regulatory expectations but also enhance transparency for investors and stakeholders.

The promotion of green finance initiatives through digital platforms represents another innovative approach. By leveraging fintech solutions, banks can facilitate access to sustainable investment opportunities, thereby driving capital towards environmentally friendly projects. This approach not only supports climate goals but also aligns with the growing demand from investors for responsible investment options.

While this review has synthesized a wealth of existing research, it has also identified several gaps that warrant further exploration. Notably, there is a need for more empirical studies that assess the real-world impact of fintech solutions on climate risk management within banks. Longitudinal studies that track the effectiveness of these technologies over time would provide valuable insights into their sustainability and scalability.

Additionally, research exploring the intersection of fintech and climate risk in emerging markets is limited. Given that many developing regions are disproportionately affected by climate change, understanding how fintech can be leveraged in these contexts is crucial. Future studies should investigate the unique challenges and opportunities that these markets present, particularly concerning data availability and regulatory frameworks.

Moreover, the ethical implications of using AI and ML in climate risk management require deeper examination. Research focused on establishing best practices for algorithmic transparency and accountability will be vital in ensuring that fintech solutions contribute positively to sustainability goals without exacerbating existing inequalities. The integration of fintech into climate risk management represents a significant opportunity for banks to enhance their resilience in the face of growing climate-related financial risks. The literature review has established that while challenges remain, the potential benefits of leveraging advanced technologies are substantial. By adopting innovative approaches, fostering collaboration, and addressing ethical considerations, banks can navigate the complexities of climate risk more effectively.

As stakeholders in the financial ecosystem—researchers, policymakers, and institutions—continue to explore this dynamic landscape, the insights gained from this review can inform strategies that contribute to a more resilient and sustainable financial system. Moving forward, a concerted effort to bridge existing gaps in the literature and practice will be essential in ensuring that the banking sector not only survives but thrives in an era increasingly defined by climate change.

References

- Arner, D., Barberis, J., Buckley, R. P. (2020). Fintech, Bigtech, and the interoperability of digital financial infrastructure. Journal of Financial Regulation, 6(2). <https://www.bis.org/publ/bppdf/bispap117.pdf>;

- Babu, R. (2024). Blockchain-Enabled Carbon Credit Trading: Revolutionizing Sustainability Efforts. International Journal of Research. Computer Applications and Information Technology (IJRCAIT), 7(2).

- Bank for International Settlements (BIS) Innovation Hub, Central Bank of the United Arab Emirates (CBUAE), Emirates Institute of Finance (EIF). (2023). Scaling climate action: Unleashing innovative technologies in sustainable finance. <https://www.bis.org/innovation_hub/projects/2023_cop28_techsprint.pdf>;

- Bartlett, R., Morse, A., Stanton, R., Wallace, N. (2019). Consumer-lending discrimination in the FinTech era. National Bureau of Economic Research. <https://faculty.haas.berkeley.edu/morse/research/papers/discrim.pdf>;

- Basel Committee on Banking Supervision. (2021). Climate-related financial risks – measurement methodologies. Basel, Switzerland: Bank for International Settlements. <https://www.bis.org/bcbs/publ/d518.pdf>;

- Bolton, P., Despres, M., Pereira da Silva, L. A., Samama, F., Svartzman, R. (2020). The green swan: Central banking and financial stability in the age of climate change. Bank for International Settlements. <https://www.bis.org/publ/othp31.pdf>.

- Dunbar, K., Sarkis, J., Treku, D. N. (2024). Fintech for environmental sustainability: promises and pitfalls. One Earth, 7(1), pp. 23-30. <https://doi.org/10.1016/j.oneear.2023.12.012>;

- Feyen, E., Frost, J., Gambacorta, L., Natarajan, H., Saal, M. (2021). Fintech and the digital transformation of financial services: implications for market structure and public policy. BIS Papers No 117. Bank for International Settlements and the World Bank Group. <https://www.bis.org/publ/bppdf/bispap117.pdf>;

- Gomber, P., Kauffman, R. J., Parker, C., Weber, B. W. (2018). On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), pp. 220-265. <https://doi.org/10.1080/07421222.2018.1440766>;

- Gosling, T. (2024). Universal Owners and Climate Change, Journal of Financial Regulation, Vol. 00, No. 00. <https://lbsresearch.london.edu/id/eprint/3972/1/fjae010.pdf>;

- International Monetary Fund. (2024, April). Navigating Climate Transitions: The Role of Financial Policies. Global Financial Stability Report. Washington, DC: International Monetary Fund;

- International Monetary Fund. (2024). Fintech and Climate Risk Management in Banking. IMF Working Paper, 24/8. Washington, DC: International Monetary Fund;

- King & Wood Mallesons. (2021). Blockchain and ESG: Blockchain for Sustainability and Green Finance;

- Kouhizadeh, M., Sarkis, J. (2020). Blockchain Practices, Potentials, and Perspectives in Greening Supply Chains. <https://iaeme.com/MasterAdmin/Journal_uploads/IJRCAIT/VOLUME_7_ISSUE_2/IJRCAIT_07_02_017.pdf>;

- Nieto, M. J. (2019). Banks, Climate Risk and Financial Stability. Journal of Financial Regulation and Compliance, 27, no. 2: 243–262. <https://doi.org/10.1108/JFRC-03-2018-0043>;

- Mhlanga, D. (2022). The role of financial inclusion and FinTech in addressing climate-related challenges in the industry 4.0: Lessons for sustainable development goals. Front. Clim. 4:949178. <DOI:10.3389/fclim.2022.949178>;

- Network for Greening the Financial System (NGFS). (2022). Final report on bridging data gaps. <https://www.ngfs.net/sites/default/files/medias/documents/final\_report\_on\_bridging\_data\_gaps.pdf>;

- Office of the Comptroller of the Currency (OCC). (2023). Semiannual Risk Perspective. <https://www.occ.gov/publications-and-resources/publications/semiannual-risk-perspective/files/pub-semiannual-risk-perspective-fall-2023.pdf>.

- Perez, C. (2002). Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages. Edward Elgar Publishing

- Singhvi, S., Dadhich, M. (2023). FinTech Revolution and Future of Sustainable Banking: Opportunities and Risks Analysis. International Journal of Management and Development Studies, vol. 12, no. 04. <DOI:10.53983/ijmds.v12n04.003>;

- The International Finance Corporation (IFC). (2023). Mapping of Digital Solutions to Support Financial Services Providers in Assessing Climate Impact on Agricultural Portfolios. <https://www.ifc.org/content/dam/ifc/doc/2024/mapping-of-digital-solutions-to-support-financial-services-providers-in-assessing-climate-impact-on-agricultural-portfolios-ifc-2023.pdf>;

- United Nations Environment Programme Finance Initiative (UNEP FI). (2024). The Climate Data Challenge: The Critical Role of Open-Source and Neutral Data Platforms. Technical Supplement to the 2024 Climate Risk Landscape Report. <https://www.unepfi.org/wordpress/wp-content/uploads/2024/05/Dataland-Final-Report-The-Climate-Data-Challenge-1.pdf>;

- Wu, Q. (2024). From bits to emissions: how FinTech benefits climate resilience? Empirical Economics. <https://doi.org/10.1007/s00181-024-02609-9>;

- Yang, Z., Nguyen T. T. H., Nguyen H. N., Nguyen T. T. N., Cao T. T. (2020). Greenwashing behaviours: Causes, taxonomy and consequences based on a systematic literature review. Journal of Business Economics and Management (JBEM), ISSN 2029-4433, Vilnius Gediminas Technical University, Vilnius, Vol. 21, Iss. 5, pp. 1486-1507. <https://doi.org/10.3846/jbem.2020.1322>.

[1] International Monetary Fund. (2024, April). Navigating Climate Transitions: The Role of Financial Policies. Global Financial Stability Report, Chapter 2. Washington, DC: International Monetary Fund.

[2] Nieto, M. J. (2019). Banks, Climate Risk and Financial Stability. Journal of Financial Regulation and Compliance, 27, no. 2: 243–262. <https://doi.org/10.1108/JFRC-03-2018-0043>.

[3] International Monetary Fund. (2024). Fintech and Climate Risk Management in Banking. IMF Working Paper, 24/8. Washington, DC: International Monetary Fund, p. 4.

[4] Ibid.

[5] Arner, D., Barberis, J., Buckley, R. P. (2020). Fintech, Bigtech, and the interoperability of digital financial infrastructure. Journal of Financial Regulation, 6(2), pp. 211-244. <https://www.bis.org/publ/bppdf/bispap117.pdf>.

[6] International Monetary Fund. (2024, April). Navigating Climate Transitions: The Role of Financial Policies. Global Financial Stability Report, Chapter 2. Washington, DC: International Monetary Fund.

[7] International Monetary Fund. (2024). Fintech and Climate Risk Management in Banking. IMF Working Paper, 24/8. Washington, DC: International Monetary Fund, p. 5.

[8] International Monetary Fund. (2024, April). Navigating Climate Transitions: The Role of Financial Policies. Global Financial Stability Report, Chapter 2. Washington, DC: International Monetary Fund.

[9] Gomber, P., Kauffman, R. J., Parker, C., Weber, B. W. (2018). On the fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), pp. 220-265. <https://doi.org/10.1080/07421222.2018.1440766>.

[10] International Monetary Fund. (2024). Fintech and Climate Risk Management in Banking. IMF Working Paper, 24/8. Washington, DC: International Monetary Fund, p. 17.

[11] Ibid., p. 1.

[12] Wu, Q. (2024). From bits to emissions: how FinTech benefits climate resilience? Empirical Economics. <https://doi.org/10.1007/s00181-024-02609-9>.

[13] Singhvi, S., Dadhich, M. (2023). FinTech Revolution and Future of Sustainable Banking: Opportunities and Risks Analysis. International Journal of Management and Development Studies, vol. 12, no. 04, pp. 12-21. <DOI:10.53983/ijmds.v12n04.003>.

[14] Cen .Y and J. Yin. (2024). Navigating Climate Challenges: Focusing on the Effectiveness of Natural Resource Rents, Fintech, Green Finance, Environmental Quality, and Digitalisation. Resources Policy 95: 105102. <https://doi.org/10.1016/j.resourpol.2024.105102>.

[15] Mhlanga, D. (2022). The role of financial inclusion and FinTech in addressing climate-related challenges in the industry 4.0: Lessons for sustainable development goals. Front. Clim. 4:949178. <DOI:10.3389/fclim.2022.949178>.

[16] Bank for International Settlements (BIS) Innovation Hub, Central Bank of the United Arab Emirates (CBUAE), Emirates Institute of Finance (EIF). (2023). Scaling climate action: Unleashing innovative technologies in sustainable finance. <https://www.bis.org/innovation_hub/projects/2023_cop28_techsprint.pdf>.

[17] The International Finance Corporation (IFC). (2023). Mapping of Digital Solutions to Support Financial Services Providers in Assessing Climate Impact on Agricultural Portfolios. <https://www.ifc.org/content/dam/ifc/doc/2024/mapping-of-digital-solutions-to-support-financial-services-providers-in-assessing-climate-impact-on-agricultural-portfolios-ifc-2023.pdf>.

[18] Ibid., Executive Summary, p. 4.

[19] Kouhizadeh, M., Sarkis, J. (2020). Blockchain Practices, Potentials, and Perspectives in Greening Supply Chains.

<https://iaeme.com/MasterAdmin/Journal_uploads/IJRCAIT/VOLUME_7_ISSUE_2/IJRCAIT_07_02_017.pdf>.

[20] Bank for International Settlements (BIS) Innovation Hub, Central Bank of the United Arab Emirates (CBUAE), Emirates Institute of Finance (EIF). (2023). Scaling climate action: Unleashing innovative technologies in sustainable finance, Part 2, Finalist showcase - U-Reg Technology.

<https://www.bis.org/innovation_hub/projects/2023_cop28_techsprint.pdf>.

[21] Ibid., p. 2.

[22] Yang, Z., Nguyen T. T. H., Nguyen H. N., Nguyen T. T. N., Cao T. T. (2020). Greenwashing behaviours: Causes, taxonomy and consequences based on a systematic literature review. Journal of Business Economics and Management (JBEM), ISSN 2029-4433, Vilnius Gediminas Technical University, Vilnius, Vol. 21, Iss. 5, pp. 1486-1507. <https://doi.org/10.3846/jbem.2020.1322>.

[23] Babu, R. (2024). Blockchain-Enabled Carbon Credit Trading: Revolutionizing Sustainability Efforts. International Journal of Research. Computer Applications and Information Technology (IJRCAIT), 7(2), pp. 228-238.

[24] Bartlett, R., Morse, A., Stanton, R., Wallace, N. (2019). Consumer-lending discrimination in the FinTech era. National Bureau of Economic Research. <https://faculty.haas.berkeley.edu/morse/research/papers/discrim.pdf>.

[25] Bank for International Settlements (BIS) Innovation Hub, Central Bank of the United Arab Emirates (CBUAE), Emirates Institute of Finance (EIF). (2023). Scaling climate action: Unleashing innovative technologies in sustainable finance, Part 2, Finalist showcase - ZERO13, p. 27. <https://www.bis.org/innovation_hub/projects/2023_cop28_techsprint.pdf>.

[26] Ibid. Finalist showcase - Triangle Solution proposed, p. 25. <https://www.bis.org/innovation_hub/projects/2023_cop28_techsprint.pdf>.

[27] Ibid., Finalist showcase -STACS Solution proposed, p. 20. <https://www.bis.org/innovation_hub/projects/2023_cop28_techsprint.pdf>.

[28] Ibid., Finalist showcase - U-Reg Technology, p. 21.

[29] Ibid., p. 2.

[30] Network for Greening the Financial System (NGFS). (2022). Final report on bridging data gaps. Section 3.2.1. <https://www.ngfs.net/sites/default/files/medias/documents/final\_report\_on\_bridging\_data\_gaps.pdf>.

[31] Ibid., Section 3.2.2.

[32] Ibid., Section 3.1.

[33] Office of the Comptroller of the Currency (OCC). (2023). Semiannual Risk Perspective. Part IV, E.

<https://www.occ.gov/publications-and-resources/publications/semiannual-risk-perspective/files/pub-semiannual-risk-perspective-fall-2023.pdf>.

[34] Ibid.

[35] United Nations Environment Programme Finance Initiative (UNEP FI). (2024). The Climate Data Challenge: The Critical Role of Open-Source and Neutral Data Platforms. Technical Supplement to the 2024 Climate Risk Landscape Report. <https://www.unepfi.org/wordpress/wp-content/uploads/2024/05/Dataland-Final-Report-The-Climate-Data-Challenge-1.pdf>.

[36] Ibid., Section 3.2.2.

[37] Ibid., p. 5.

[38] The International Finance Corporation (IFC). (2023). Mapping of Digital Solutions to Support Financial Services Providers in Assessing Climate Impact on Agricultural Portfolios. <https://www.ifc.org/content/dam/ifc/doc/2024/mapping-of-digital-solutions-to-support-financial-services-providers-in-assessing-climate-impact-on-agricultural-portfolios-ifc-2023.pdf>.

[39] Bank for International Settlements (BIS) Innovation Hub, Central Bank of the United Arab Emirates (CBUAE), Emirates Institute of Finance (EIF). (2023). Scaling climate action: Unleashing innovative technologies in sustainable finance, Part 2, Finalist showcase - Triangle Solution proposed, p. 25. <https://www.bis.org/innovation\_hub/projects/2023\_cop28\_techsprint.pdf>.

[40] Ibid., p. 24.

[41] Ibid., Part 2, Finalist showcase - ZERO13, p. 27.

[42] The International Finance Corporation (IFC). (2023). Mapping of Digital Solutions to Support Financial Services Providers in Assessing Climate Impact on Agricultural Portfolios.

<https://www.ifc.org/content/dam/ifc/doc/2024/mapping-of-digital-solutions-to-support-financial-services-providers-in-assessing-climate-impact-on-agricultural-portfolios-ifc-2023.pdf>.

[43] Feyen, E., Frost, J., Gambacorta, L., Natarajan, H., Saal, M. (2021). Fintech and the digital transformation of financial services: implications for market structure and public policy. BIS Papers No 117. Bank for International Settlements and the World Bank Group. <https://www.bis.org/publ/bppdf/bispap117.pdf>.

[44] Bolton, P., Despres, M., Pereira da Silva, L. A., Samama, F., Svartzman, R. (2020). The green swan: Central banking and financial stability in the age of climate change. Bank for International Settlements. Abstract, Executive Summary, Chapter 1 (pp. 1-10), Chapter 3 (pp. 23-46), Chapter 4 (pp. 47-64), Chapter 5 (pp. 65-67), Annex 2 (pp. 72-78). <https://www.bis.org/publ/othp31.pdf>.

[45] Ibid., Chapter 4.5, p. 63.

[46] Gosling, T. (2024). Universal Owners and Climate Change, Journal of Financial Regulation, Vol. 00, No. 00, pp. 1–40. <https://lbsresearch.london.edu/id/eprint/3972/1/fjae010.pdf>.

[47] Ibid., p.15.

[48] Basel Committee on Banking Supervision. (2021). Climate-related financial risks – measurement methodologies. Basel, Switzerland: Bank for International Settlements. Sections 2.2, 3.2, 4.1.2, 4.2.1, and Executive Summary. <https://www.bis.org/bcbs/publ/d518.pdf>.

[49] Network for Greening the Financial System (NGFS). (2022). Final report on bridging data gaps. Section 3.2.1.

<https://www.ngfs.net/sites/default/files/medias/documents/final\_report\_on\_bridging\_data\_gaps.pdf>.

[50] Feyen, E., Frost, J., Gambacorta, L., Natarajan, H., Saal, M. (2021). Fintech and the digital transformation of financial services: implications for market structure and public policy. BIS Papers No 117. Bank for International Settlements and the World Bank Group. <https://www.bis.org/publ/bppdf/bispap117.pdf>.

[51] United Nations Environment Programme Finance Initiative (UNEP FI). (2024). The Climate Data Challenge: The Critical Role of Open-Source and Neutral Data Platforms. Technical Supplement to the 2024 Climate Risk Landscape Report. <https://www.unepfi.org/wordpress/wp-content/uploads/2024/05/Dataland-Final-Report-The-Climate-Data-Challenge-1.pdf>.

[52] Office of the Comptroller of the Currency (OCC). (2023). Semiannual Risk Perspective, Part IV, E. <https://www.occ.gov/publications-and-resources/publications/semiannual-risk-perspective/files/pub-semiannual-risk-perspective-fall-2023.pdf>.

[53] Bolton, P., Despres, M., Pereira da Silva, L. A., Samama, F., Svartzman, R. (2020). The green swan: Central banking and financial stability in the age of climate change. Bank for International Settlements. Abstract, Executive Summary, Chapter 1 (pp. 1-10), Chapter 3 (pp. 23-46), Chapter 4 (pp.47-64), Chapter 5 (pp. 65-67), Annex 2 (pp. 72-78). <https://www.bis.org/publ/othp31.pdf>.

[54] Ibid., Chapter 4.5, p. 63.

[55] Dunbar, K., Sarkis, J., Treku, D. N. (2024). Fintech for environmental sustainability: promises and pitfalls. One Earth, 7(1), pp. 23-30. <https://doi.org/10.1016/j.oneear.2023.12.012>.

Downloads

Downloads

Published

Issue

Section

License

Copyright (c) 2026 Rym Bouchelit, Abdelkader Belarbi (Author)

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

How to Cite

Share